For years, pharmaceutical outsourcing decisions involving India have carried an old qualification: the country offers cost advantages, but its quality systems may be stronger elsewhere. That view no longer reflects the structure of India’s pharmaceutical industry or the evidence from regulated markets. India’s pharmaceutical products now reach approximately 200 countries and territories, while its manufacturers supply about 20% of the world’s generic medicines by volume.1,2

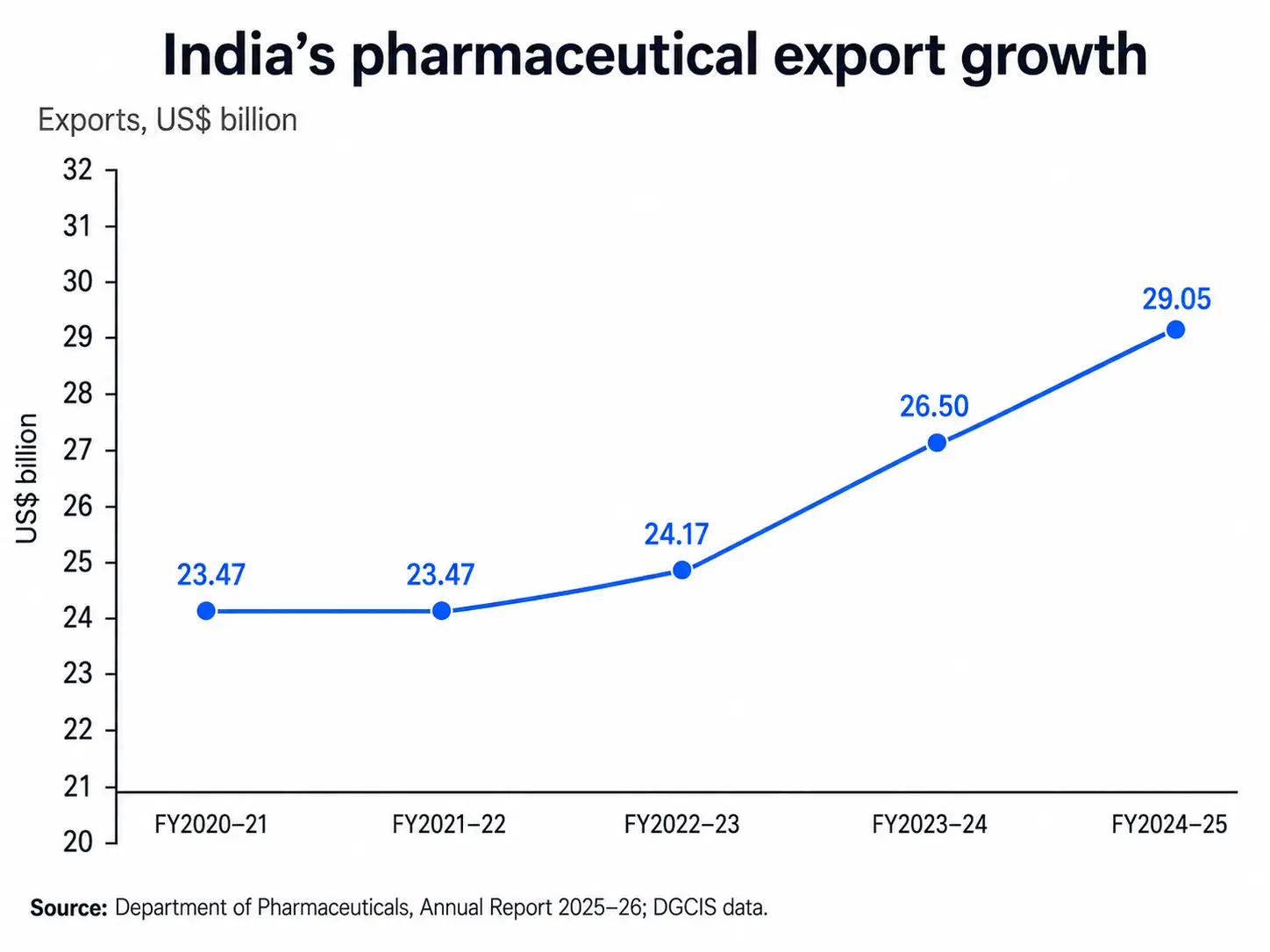

Pharmaceutical exports reached approximately US$29 billion, or ₹2.46 trillion, in FY2024–25.2 This scale is supported by sustained participation in regulated markets, repeated inspections, and quality systems designed for global development and commercial supply.

The same progression is visible in contract research, development, and manufacturing. A 2025 BCG–IPSO industry study estimated that India’s innovation-led CRDMO sector grew from US$1.4–1.8 billion in 2019 to US$3–3.5 billion in 2024, representing annual growth of about 15%, compared with global growth of 7%–8%.3

India’s rise is therefore not simply a low-cost manufacturing story. It reflects a broader shift toward scientific services, integrated development, regulated manufacturing, and complex modalities.

Pharmaceutical manufacturing compliance and the quality perception

The quality concern is not entirely invented. Indian facilities have received US FDA warning letters, import alerts, and adverse inspection findings. Some failures have involved serious issues such as data integrity, inadequate investigations, weak contamination controls, and poor corrective and preventive action systems.

Those failures should not be minimized. However, using them to judge the entire Indian pharmaceutical sector creates a misleading comparison. Manufacturing facilities in the United States, Europe, China, and other regions also receive regulatory observations. The relevant questions are how frequently a manufacturing base is inspected, what proportion of inspected sites remain outside formal regulatory action, and whether companies continue to improve their quality systems.

Inspection intensity and facility classifications

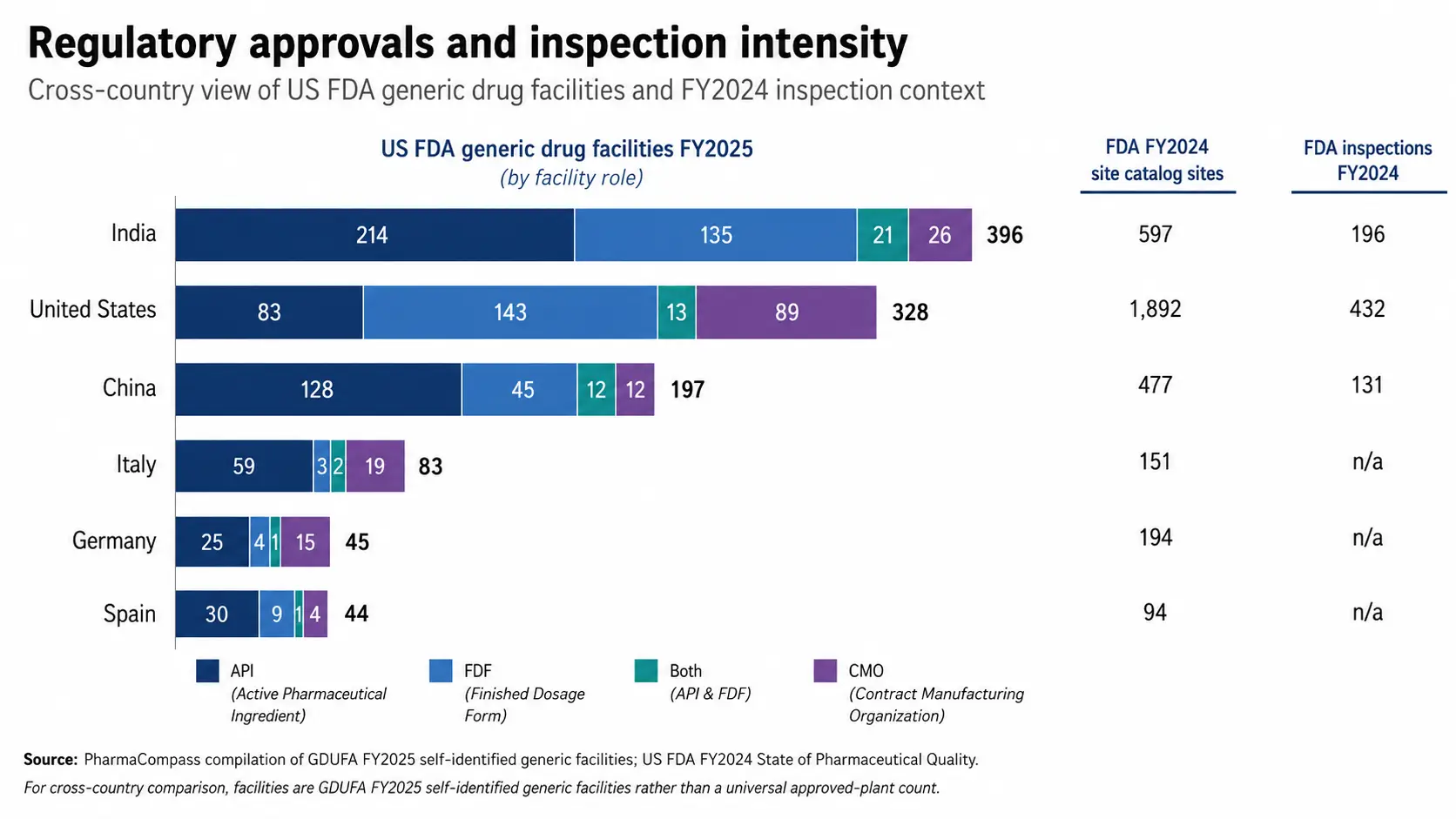

The FDA’s FY2024 pharmaceutical quality report provides a useful view. During the year, 34% of Indian sites in the agency’s catalog were inspected, compared with 28% of sites in China and 24% of sites in the United States. India was therefore subject to greater inspection coverage than either comparator.4

The scale of India’s regulated manufacturing base is also evident in the number and types of facilities participating in the US generic drug supply chain. GDUFA FY2025 data compiled by PharmaCompass show that India had 396 self-identified generic drug facilities, more than the United States, China, Italy, Germany, or Spain. Of these, 214 were API facilities and 135 were finished dosage form facilities, reflecting strength across both drug substance and drug product manufacturing.5,6

Figure 1. India leads major pharmaceutical markets in US FDA generic drug facilities, supported by broad API, finished dosage form, and contract manufacturing capacity.

The two datasets in Figure 1 measure different aspects of regulatory presence. The GDUFA figures show self-identified generic drug facilities by manufacturing role, while the FDA site catalog and inspections indicate the broader scale of sites under FDA oversight and the intensity of inspections during FY2024. They should not be read as universal counts of “FDA-approved plants.” Together, however, they show that India combines a large, regulated manufacturing base with substantial inspection exposure.

Among sites with an inspection history, 87% of Indian facilities had a latest classification of either no action indicated or voluntary action indicated, compared with 93% in China and 92% in the United States.4 This should not be presented as evidence that India has no quality gap. It does show that the large majority of inspected Indian sites were not under an official action classification.

The honest conclusion is more useful than extreme. India is not free of compliance problems, but neither is it a low-oversight manufacturing geography. It operates under intensive scrutiny, and leading Indian CRDMOs have built quality systems for programs intended for the United States, Europe, Japan, the United Kingdom, Canada, and other regulated markets.

India’s pharmaceutical industry: Scale and evidence of trust

Export volume alone cannot prove that every manufacturer meets the same standard. It does, however, show that Indian companies have repeatedly qualified to participate in global supply chains where regulatory filings, batch records, analytical controls, change management, and traceability are mandatory.

The Department of Pharmaceuticals reports that India meets nearly 40% of US generic medicine demand and approximately 25% of medicine demand in the United Kingdom. Indian manufacturers also account for 60% of the vaccines supplied to UNICEF.2

These markets do not accept products simply because they are inexpensive. Manufacturers must establish product quality, pharmaceutical manufacturing compliance, reliable release testing, and continuity of supply. A company may still fail an inspection, but sustained participation across thousands of products and multiple jurisdictions cannot be explained by cost alone.

Figure 2. India’s pharmaceutical exports rose from US$23.47 billion in FY2020–21 to US$29.05 billion in FY2024–25, reflecting sustained global demand.

The export trend is important, but the composition of the industry is changing as well. India is moving beyond high-volume generics toward discovery research, development services, clinical supply, complex active ingredients, biologics, peptides, antibody–drug conjugates, and commercial manufacturing.

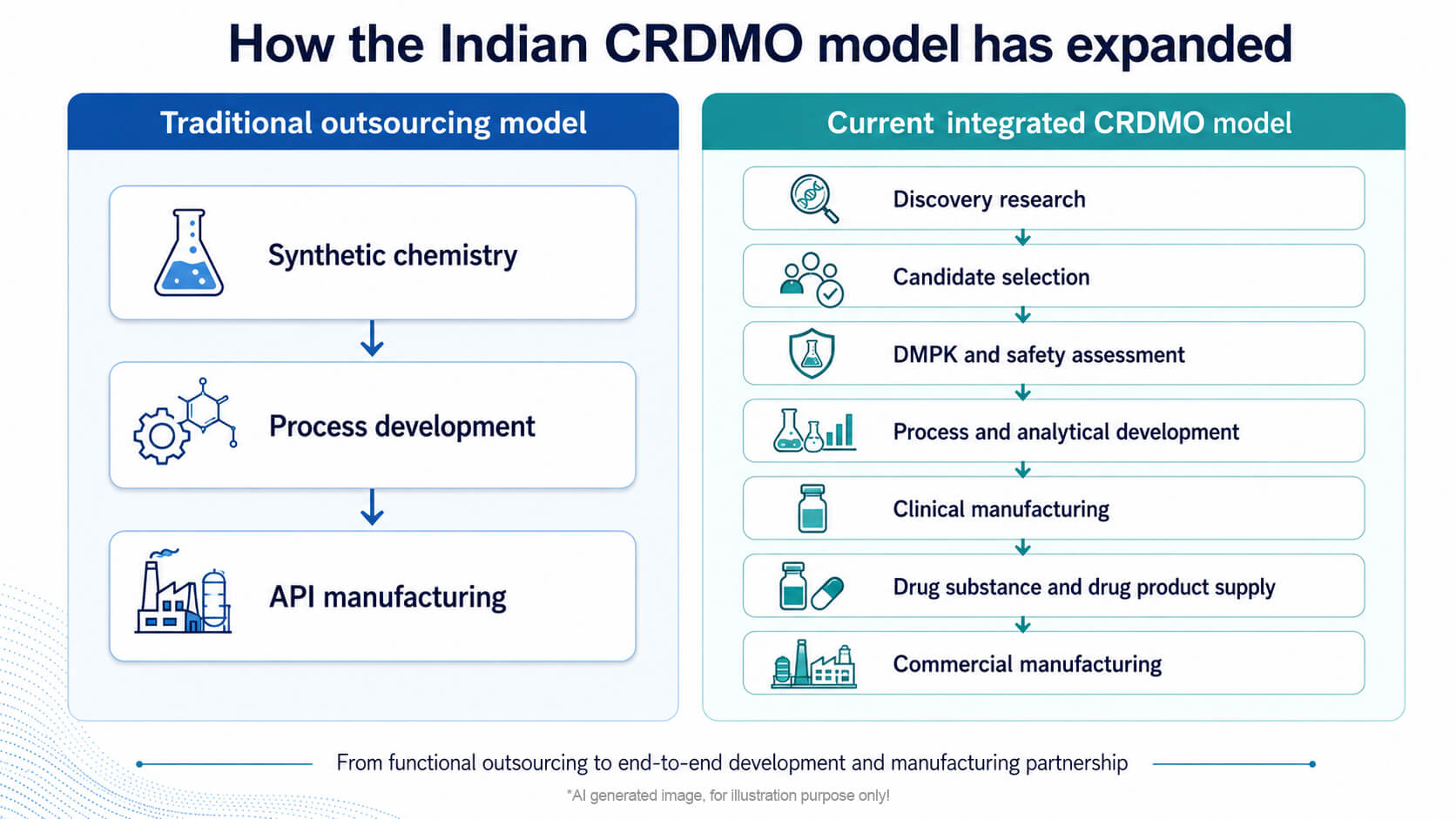

From pharmaceutical outsourcing to integrated CRDMO programs

India’s early pharmaceutical outsourcing advantage was built largely on synthetic chemistry, process development, and active pharmaceutical ingredient manufacturing. Those strengths remain important, particularly for small molecules. The difference today is that leading companies can support a much larger portion of the molecule’s journey.

An integrated Indian CRDMO may now contribute to medicinal chemistry, in vitro biology, DMPK, toxicology, formulation, analytical method development, process scale-up, clinical manufacturing, and commercial supply. For biologics, the service chain can extend from cell line and process development through upstream and downstream manufacturing, analytical characterization, and fill-finish.

This development model has practical value. Moving a program between unrelated vendors can result in repeated method transfer, fragmented documentation, loss of process knowledge, and unclear accountability. An integrated partner can retain scientific context as the molecule progresses, although integration is valuable only when the individual functions are technically strong and governed by robust quality systems.

Figure 3. India’s CRDMO sector has evolved from standalone chemistry and API services to integrated discovery, development, clinical supply, and commercial manufacturing.

The market data reflect this transition. BCG and the Indian Pharmaceutical Services Organisation estimate that India’s innovation-led CRDMO sector expanded at approximately 15% annually between 2019 and 2024.3 Their definition excludes several lower-value or adjacent service categories, which is why some other market reports provide larger estimates. The useful point is not the exact market-size label. It is the direction and rate of growth.

Cost remains relevant, but it is not enough

India continues to offer lower operating and talent costs than many Western locations. Ignoring that advantage would be unrealistic. However, cost by itself does not win complex development programs. A failed batch, delayed technology transfer, weak investigation, or poorly controlled analytical method can erase the savings from a lower initial quotation. Buyers increasingly assess the total cost and risk of delivery rather than comparing hourly rates alone.

The stronger Indian CRDMOs compete through a combination of scientific depth, capacity, speed, and continuity. Their value lies in deploying larger multidisciplinary teams, starting projects quickly, maintaining close interaction between functions, and moving successful processes toward scale without repeatedly changing partners.

This is particularly relevant for venture-backed biotechnology companies, which may not have internal infrastructure for every stage of development. It is also useful to large pharmaceutical companies seeking additional capacity or geographic diversification without building new facilities for every program.

Biologics manufacturing investment is changing the capability mix

The growth of biologics provides one of the clearest tests of whether India can move beyond its traditional small-molecule base. Biologics manufacturing requires substantial capital, specialized facilities, contamination control, process consistency, complex analytics, experienced quality oversight, and mature quality systems. It cannot be built on labor-cost advantage alone.

Recent investments show that Indian CRDMOs are developing this capability. Syngene’s FY2024–25 annual report states that the company operationalized an additional 20,000 L of biologics drug-substance capacity in Bengaluru, together with a commercial-scale, high-speed fill-finish unit. Its acquisition of a biologics facility in Baltimore subsequently increased its total single-use bioreactor capacity to 50,000 L across its network.7

The significance is not the capacity number by itself. Syngene’s model links discovery and development expertise in India with clinical and commercial manufacturing infrastructure. This allows process knowledge to remain connected across stages and gives clients access to manufacturing in more than one geography. This type of strategic outsourcing is increasingly relevant for biologics companies that need specialized capacity but do not want to build and maintain every capability internally.

Other Indian companies are also adding mammalian, microbial, continuous biomanufacturing, and fill-finish capacity. These investments remain uneven across the industry, and India still has gaps in areas such as advanced biologics talent, very large-scale mammalian manufacturing, and some new modalities. Nevertheless, capital deployment is moving decisively toward higher-complexity work.

Why Syngene fits naturally into the India story

Syngene is relevant to this discussion because its evolution mirrors the broader change in India’s CRDMO sector. It began with research services and has expanded across discovery, development, small-molecule manufacturing, biologics manufacturing, and other specialized capabilities.

Its advantage is not merely that these services exist within the same company. The stronger argument is that scientific and process knowledge can move with the program. Discovery teams can work with development scientists earlier, analytical considerations can enter process decisions sooner, and manufacturing risks can be examined before a program reaches late-stage transfer.

Syngene also provides a practical answer to the geographic-risk question. Its Indian operations offer scientific depth and scalable infrastructure, while its expanding international network provides additional manufacturing options. That combination is increasingly relevant as clients look for both integration and supply-chain diversification.

The company should not be treated as proof that every Indian provider offers the same quality or breadth. It is better understood as an example of the upper end of the Indian CRDMO market: scientifically integrated, capital-intensive, globally inspected, and built for long-term partnerships rather than isolated service transactions.

What quality systems should global sponsors examine?

The debate should now move beyond whether India, as a country, can deliver quality. Country-level labels are too broad to support a serious outsourcing decision. Sponsors need to evaluate the specific organization, site, team, and quality system involved.

That means examining regulatory history, investigation quality, data governance, employee turnover, technical depth, technology-transfer controls, supply-chain resilience, cybersecurity, environmental performance, and the provider’s record in the required modality. A strong national industry does not remove the need for vendor qualification.

Sponsors should also examine whether quality systems operate consistently across discovery, development, technology transfer, and manufacturing rather than appearing only at the GMP stage. Documentation practices, deviation management, CAPA effectiveness, data integrity controls, and management oversight reveal more than broad claims about quality culture.

The quality myth becomes dangerous in both directions. Assuming that Indian providers are inherently weak can cause companies to overlook capable partners. Assuming that every Indian provider is equally strong can expose a program to avoidable risk.

The correct approach is evidence-based selection.

India’s opportunity is real, but not guaranteed

India has the scientific base, manufacturing experience, cost structure, and regulatory exposure needed to become a larger global CRDMO center. The sector is growing faster than the global market, and customer demand for geographic diversification is creating a favorable opening.

However, growth will depend on maintaining quality while capacity expands. Companies will need to invest in experienced technical leadership, modern digital systems, stronger investigation practices, advanced-modality skills, environmental controls, and a culture in which production pressure does not override scientific judgment.

The companies that do this well will not be chosen because they are Indian or because they are inexpensive. They will be chosen because their quality systems support sound scientific decisions, reliable process transfer, rigorous documentation, and consistent delivery against specification.

India has already moved beyond the role of a secondary outsourcing location. Its strongest CRDMOs are becoming integrated contributors to global drug discovery, development, and manufacturing. The remaining quality debate should therefore be based on site-level evidence, not an outdated national stereotype.

References

- Bain & Company, Indian Pharmaceutical Alliance, Pharmaceuticals Export Promotion Council of India, and Indian Drugs Manufacturers Association. Healing the World: A Roadmap for Making India a Global Pharma Exports Hub. 2025.

- Department of Pharmaceuticals, Ministry of Chemicals and Fertilizers, Government of India. Annual Report 2025–26. Government of India; 2026.

- Agarwalla V, Suryaprakash S, Mathur S, et al. Unleashing the Tiger: Indian CRDMO Sector 2025. Boston Consulting Group and Indian Pharmaceutical Services Organisation; 2025.

- US Food and Drug Administration, Office of Pharmaceutical Quality. Report on the State of Pharmaceutical Quality, FY2024. FDA; 2025.

- PharmaCompass. Chinese FDA-registered generic facilities gain steam, India maintains lead with 396 facilities. Radio Compass Blog. 2024.

- US Food and Drug Administration. FY2025 Self-Identified Generic Drug Facilities, Sites and Organizations. FDA.

- Syngene International Limited. Annual Report 2024–25: Innovating Reach. Syngene International Limited; 2025.